Introduction: After a four-year slump, AIA Group Ltd. (HKSE: 1299) is showing signs of a comeback. The Hong Kong–based life insurance giant – the largest in Asia-Pacific – saw its stock languish from 2019 through 2023, weighed down by pandemic disruptions and economic uncertainties. Now, early indicators point to a rebound in both share priceand business performance, making it a compelling time to revisit AIA’s investment case. The company’s latest 1H 2024 results highlight surging new business growth, rising profits, and hefty shareholder returns, all while the stock remains undervalued. Let’s dive into the key points of this thesis and why AIA presents an attractive opportunity for investors.

Recent Stock Performance: Turning the Corner After a Multiyear Downtrend

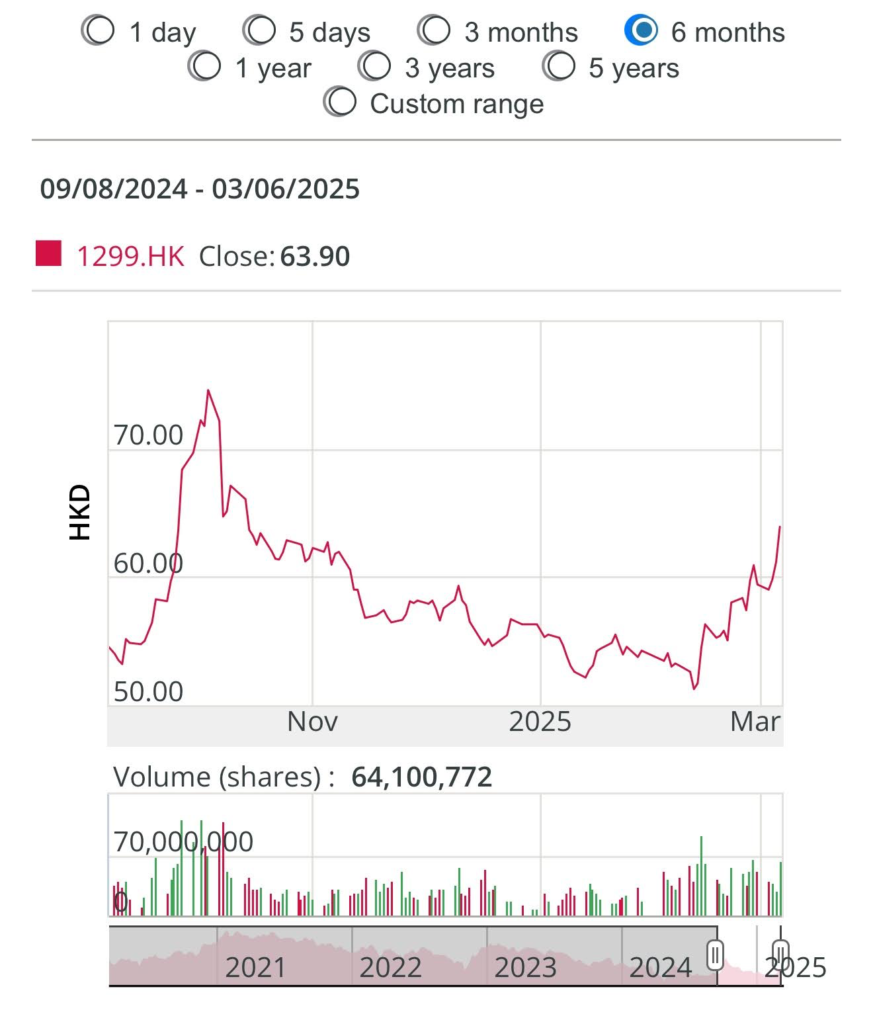

AIA Group’s stock price has started to recover from a multi-year decline, as shown in the chart above. After peaking in 2019, AIA’s share price entered a prolonged downtrend, exacerbated by COVID-19 lockdowns and market volatility. By late 2022, the stock had fallen significantly. However, in recent months AIA’s price has climbed off its lows, suggesting that investor sentiment is improving. The early rebound (with shares up from ~HK$50s to mid-$60s) hints that the market is beginning to recognize AIA’s strengthening fundamentals. This trend reversal provides a favorable backdrop – buying into a quality company just as momentum turns positive.

1H 2024 Highlights: Strong Financial Growth

AIA’s interim 2024 results showed impressive growth, signaling a robust post-pandemic recovery in its core metrics:

- Value of New Business (VONB): US$2.455 billion (record high, +25% YoY growth)ipmiglobal.com. This measures the present value of expected profits from new policies sold – a key gauge of sales momentum.

- Operating Profit After Tax (OPAT): US$3.386 billion (+10% per share YoY)ipmiglobal.com, reflecting double-digit earnings growth.

- Operating Return on Equity (ROE): 15.3%, up from 13.5% last yearipmiglobal.com, demonstrating improved profitability and efficient capital use.

What this means: AIA is firing on all cylinders financially. Surging VONB indicates robust new sales – the lifeblood for a life insurer’s future earnings – and at higher profitability. OPAT growth in the double digits (even on a per-share basis) shows that core earnings are expanding healthily, not just top-line sales. Importantly, the rise in ROE to 15.3% means AIA is generating higher returns on shareholders’ equity than before

, a sign of strengthening business quality (Source: ipmiglobal.com, 2025). In short, AIA delivered record new business and strong profit growth in 1H24, affirming that the company has bounced back from the challenges of the past few years.

Capital Strength and Shareholder Returns

AIA pairs its earnings growth with a fortress balance sheet and generous returns to shareholders:

- Free Surplus: US$14.6 billion in free surplus (excess capital), underpinning a robust 242% shareholder capital coverage ratio (Source: aia.com, 2025). This means AIA holds well over double the required capital – a huge safety buffer and war chest for growth or buybacks.

- Share Buyback Program: US$12.0 billion authorized for buy-backs (over 3 years), with about US$3.1 billion remaining to be executed (Source: aia.com, 2025). The company bought back $3.4 billion worth in the first half alone, and the program runs through April 2025.

- Dividend Growth: Interim dividend raised to 44.50 HK cents per share (a +5% increase) (Source: aia.com, 2025). AIA has consistently grown its dividend, and 1H24 is no exception, reflecting confidence in future cash flows.

- New Payout Policy: Introduced an enhanced capital management policy targeting a 75% payout ratio of annual net free surplus generation (through dividends + buybacks) starting in 2024 (Source: spglobal.com, 2024). In other words, AIA plans to return three-quarters of its free cash to shareholders, a notably shareholder-friendly stance.

Why this matters: AIA’s financial strength is evident – a high capital ratio and large surplus mean it can easily withstand market shocks or regulatory changes, while still investing in growth. Yet rather than hoard this excess capital, management is proactively returning money to shareholders. The hefty buybacks (US$12b program) reduce share count and boost per-share metrics, essentially giving owners a bigger slice of the pie. Dividend increases provide a growing income stream for investors. And the new 75% payout target signals that AIA will continue to distribute the bulk of its surplus cash every year

(Source: spglobal.com, 2025). This combination of balance sheet resilience and shareholder returns makes AIA stand out – investors get the best of both worlds (safety and rewards). It’s a vote of confidence by management in AIA’s prospects, and it can support the stock price (buybacks create buying demand, dividends attract yield-focused buyers).

Market Expansion and Distribution Growth

AIA’s growth is broad-based across regions and sales channels, underscoring effective execution of its expansion strategy:

- Geographic Strength: Key markets delivered outstanding new business growth in 1H24 – Mainland China VONB +36% YoY, Hong Kong VONB +26% YoY(with strong demand from both local and mainland visitor customers), and solid rebounds across Southeast Asia (for example, Thailand +16% VONB). AIA reported double-digit VONB growth in 15 out of 18 markets, illustrating that momentum is widespread, not just a one-market story.

- Agency Channel: AIA’s proprietary Premier Agency salesforce (its army of insurance agents) continues to be a powerhouse. Agency-derived VONB grew ~19% in 1H24, fueled by a surge in new recruits (+22% new agents) joining AIA. More agents and higher productivity per agent are driving sales. (Notably, AIA remains #1 globally in Million Dollar Round Table agents, reflecting its top-tier agency quality.)

- Partnership Channels: The bancassurance and broker partnerships saw VONB jump +43% YoY. Bancassurance (selling insurance through bank partners) was especially strong, as AIA leveraged large bank customer bases (e.g. new bancassurance deals in Thailand and Southeast Asia) to boost sales.

Growth drivers: These results show AIA capitalizing on market reopenings and expansion initiatives. Hong Kong’s big jump was aided by the return of mainland Chinese visitors after border reopenings, while China’s stellar 36% growth reflects rising demand as AIA expands into new cities (Source: aia.com, 2025)

In Southeast Asia, AIA’s long-term investments in distribution (like its partnership with Bangkok Bank in Thailand, Citibank in various markets, etc.) are paying off. The agency channel – AIA’s crown jewel – not only rebounded but grew its ranks by over 20%, which bodes well for future sales capacity. Likewise, the diversified distribution strategy(agency and partnerships) is delivering twin-engine growth. The takeaway: AIA is successfully growing its footprint across Asia, gaining market share, and reaching more customers than ever before through multiple channels.

Product and Customer Strategy

AIA’s focus on high-quality growth is evident in its product mix and customer acquisition strategy:

- New Customers: Nearly 1 million new customers were acquired in the first half of 2024 (around +13% vs. 1H23). This influx of new policyholders expands AIA’s base for future cross-selling and repeat business. (AIA now serves over 40 million individual policies across Asia.)

- High-Margin Products: The company emphasized sales of unit-linked and other high-margin products, which boosted the overall new business margin to 53.9% (up 3.3 pps). In plain English, AIA earned more profit per dollar of new premium – a testament to selling a richer mix of products that generate higher returns. For example, demand for investment-linked policies and protection plans (as opposed to low-margin savings products) drove profitability up.

- Attractive Economics: The internal rate of return (IRR) on new business investment exceeds 20%, with a payback period of around 3 years. This means the money AIA spends to write new policies is yielding very high returns quickly – a sign of exceptional value creation.

Why it’s important: AIA isn’t chasing growth for growth’s sake; it’s targeting quality growth. Acquiring 1 million new customers in six months is impressive, but equally important is what they are selling. By steering product mix toward higher-margin categories, AIA ensures that its VONB growth translates into disproportionately higher future profits. A 53.9% VONB margin is among the best in the industry, indicating strong pricing power and product appeal. The >20% IRR on new business highlights that AIA’s new policies are extremely profitable investments – few insurers achieve such returns on capital. This all bodes well for sustainable earnings growth. Moreover, adding lots of new customers now not only boosts immediate sales, but also expands the pool for long-term policy renewals and upselling (think riders, top-ups, health and wellness programs). Overall, AIA’s strategy of focusing on value (margin, IRR) over just volume sets it up for high-quality, long-term growth.

Future Growth Outlook

Looking ahead, AIA’s management is bullish on sustaining growth, and the company’s fundamentals support this optimism:

- Earnings Growth Guidance: AIA is targeting 9%–11% compound annual growth in OPAT per share from 2023 to 2026. This guidance, provided by management, essentially promises high-single to low-double-digit earnings growth each year – an ambitious yet achievable goal given recent momentum.

- Resilience to Market Volatility: The business has relatively low sensitivity to market swings. AIA’s large and well-diversified investment portfolio (average credit rating A) and its robust capital position help insulate it from interest rate spikes or equity market dips. In 3Q 2024, despite volatile markets, AIA’s solvency and financial metrics remained solid. This stability means the company can stay the course on growth plans without getting knocked off track by short-term market fluctuations.

- Dividend Upside: With profits rising and a 75% payout policy in place, dividends are poised to grow in tandem with earnings. Investors can reasonably expect high-single-digit or better dividend increases annually (indeed total dividends per share rose 5% in FY2023 and another 5% at the interim). Strong cash generation and surplus capital make ongoing dividend growth highly likely, adding to the stock’s total return potential.

Big picture: AIA’s outlook appears bright and confident. The 9–11% EPS growth target, if met, would compound to substantial earnings by 2026 – and management has a track record of delivering on guidance. This growth will be driven by the very factors seen in 1H24: expanding distribution, penetrating new cities in China, a growing affluent customer base in Asia, and continuous product innovation. The secular trends are on AIA’s side as well: Asia’s middle class is growing, insurance penetration is still relatively low in many markets, and consumers are increasingly seeking health and life protection. AIA, with its leading brand and scale in 18 markets, is in prime position to capture this structural growth. Meanwhile, its prudent risk management and huge capital buffer (242% capital ratio) provide downside protection, so it can grow through economic cycles without jeopardy. For investors, this means AIA offers a rare combo of growth plus defensive stability – a valuable trait in uncertain times.

DCF Valuation: Significant Upside Potential

Despite these strengths, AIA’s stock price has yet to fully reflect the company’s intrinsic value. Our discounted cash flow (DCF) valuation indicates that AIA is trading at a sizable discount:

- Current Stock Price: ~HK$64 (recent market price per share, as of early 2025).

- Estimated Fair Value (DCF): ~HK$93 per share (our calculated intrinsic value).

- Margin of Safety: ~31% (the current price is about 31% below fair value, implying substantial upside if the market corrects this undervaluation).

- Enterprise Value: ~HK$1.02 trillion (total firm value based on DCF).

- Equity Value: ~HK$990 billion (after subtracting debt, etc., the value attributable to shareholders).

- Shares Outstanding: ~10.65 billion. Fair Value per Share ≈ HK$93 (HK$990b equity / 10.65b shares).

Interpretation: In essence, the stock is undervalued. At HK$64, investors are paying roughly 0.7x our estimated value – a notable discount for a company of AIA’s caliber. A 31% margin of safety provides a cushion; even if our assumptions are slightly off, there’s room for error. This valuation gap could close as AIA continues to execute well and as investors gain confidence in its growth (or if market conditions improve in its key regions). It’s also telling that independent analysts reach similar conclusions – for instance, Goldman Sachs recently reiterated a HK$93 target price for AIA shares source: thestandard.com.hk, 2025) , aligning with our DCF-based estimate. The bottom line is that AIA’s current price does not appear to reflect its true worth or future earnings power. This presents an opportunity to buy a quality business at a discounted price.

Why AIA is an Attractive Investment Opportunity

In summary, AIA offers a compelling investment case right now: a leading franchise with accelerating growth, shareholder-friendly capital returns, and an undervalued stock. After a tough few years, AIA has emerged stronger – growing new business value at double-digit rates and setting record highs. The company’s entrenched position in Asia’s high-growth markets (China, Southeast Asia, etc.), combined with its powerhouse agency force and strategic bank partnerships, give it sustainable competitive advantages and a long runway for expansion. Meanwhile, investors are rewarded along the way via rising dividends and aggressive share buybacks, supported by AIA’s rock-solid balance sheet.

Importantly, the recent uptick in the stock price off multi-year lows could be the start of a more prolonged re-rating. As the market recognizes AIA’s consistent delivery (and as pandemic/macro clouds continue to clear), there is potential for the stock’s valuation multiples to improve. Given the ~30% margin of safety in the price, the risk/reward skews favorably. You’re essentially getting a growth stock at a value price – a rare find.

Of course, no investment is without risks (macroeconomic swings in Asia, regulatory changes, etc.), but AIA’s resilience and prudent management mitigate many of these concerns. The company navigated the pandemic and low-rate environment and still grew its embedded value and profits; it is well-equipped to handle future challenges.

Conclusion: With earnings on an upswing, ample capital to invest and return, and a discounted valuation, AIA Group looks poised to deliver attractive returns to long-term investors. The early signs of a stock rebound add a timely catalyst to what is fundamentally a high-quality, growth-driven business. For those looking to tap into Asia’s rising insurance demand through a proven market leader, AIA presents an opportunity that is hard to ignore. In investing, buying a great company after a period of weakness – just as trends turn upward – can be a recipe for outsized gains. AIA appears to fit that mold today, making it an appealing addition to a growth or dividend portfolio.

(Disclosure: This analysis is for educational purposes and reflects the author’s opinion, not investment advice. Investors should conduct their own due diligence.)